With the Financial Conduct Authority's (FCA) new Consumer Duty regulations coming into force in July 2023, financial services firms in the automotive industry are facing increased scrutiny over how they treat their customers.

Consumer Duty introduces new rules for dealers and lenders to follow aimed at delivering good outcomes for retail customers. In this post, we will look at the Consumer Principle, the new Cross-Cutting Rules, the Four Outcomes, Key Milestones, and how iVendi's solutions can help.

The FCA's Consumer Duty is a new set of rules created to improve how financial services firms treat their customers. The new Duty "sets higher and clearer standards of consumer protection across financial services, and requires firms to put their customers’ needs first." All financial service providers that are regulated by the FCA and offer products or services to consumers must follow these rules.

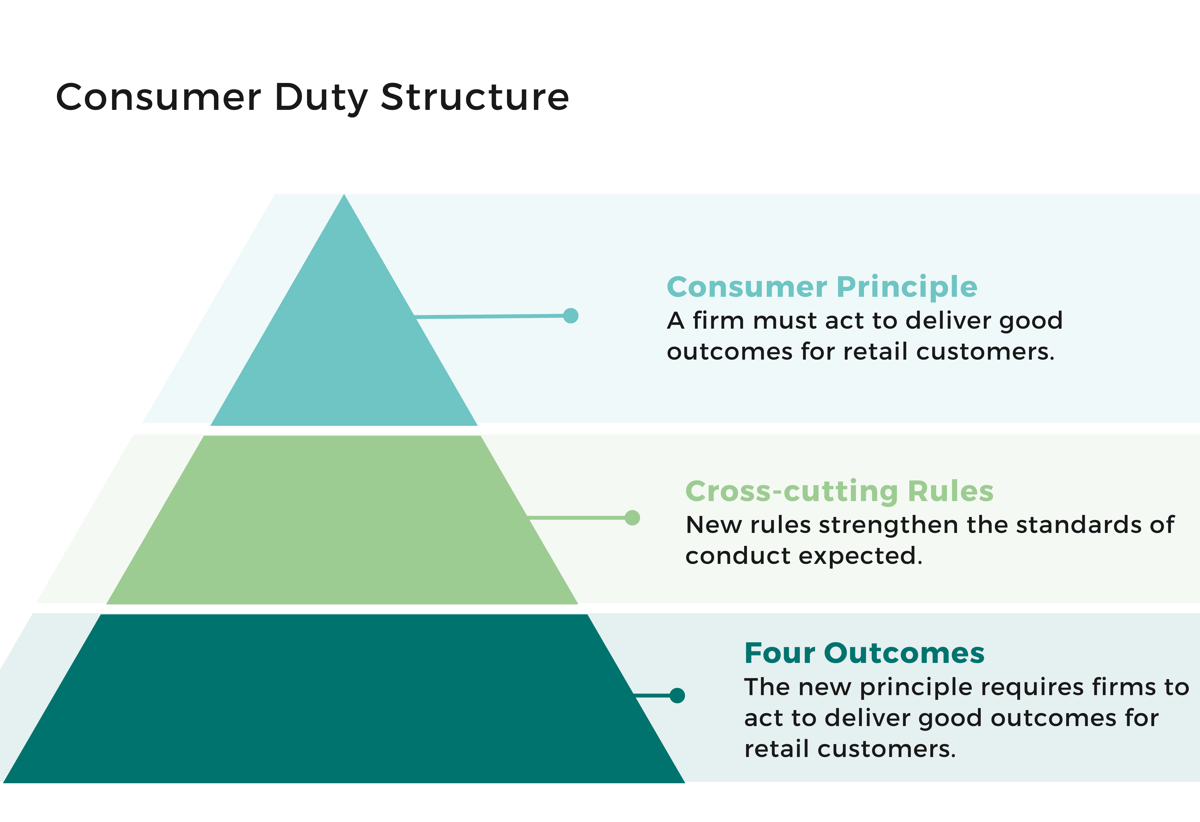

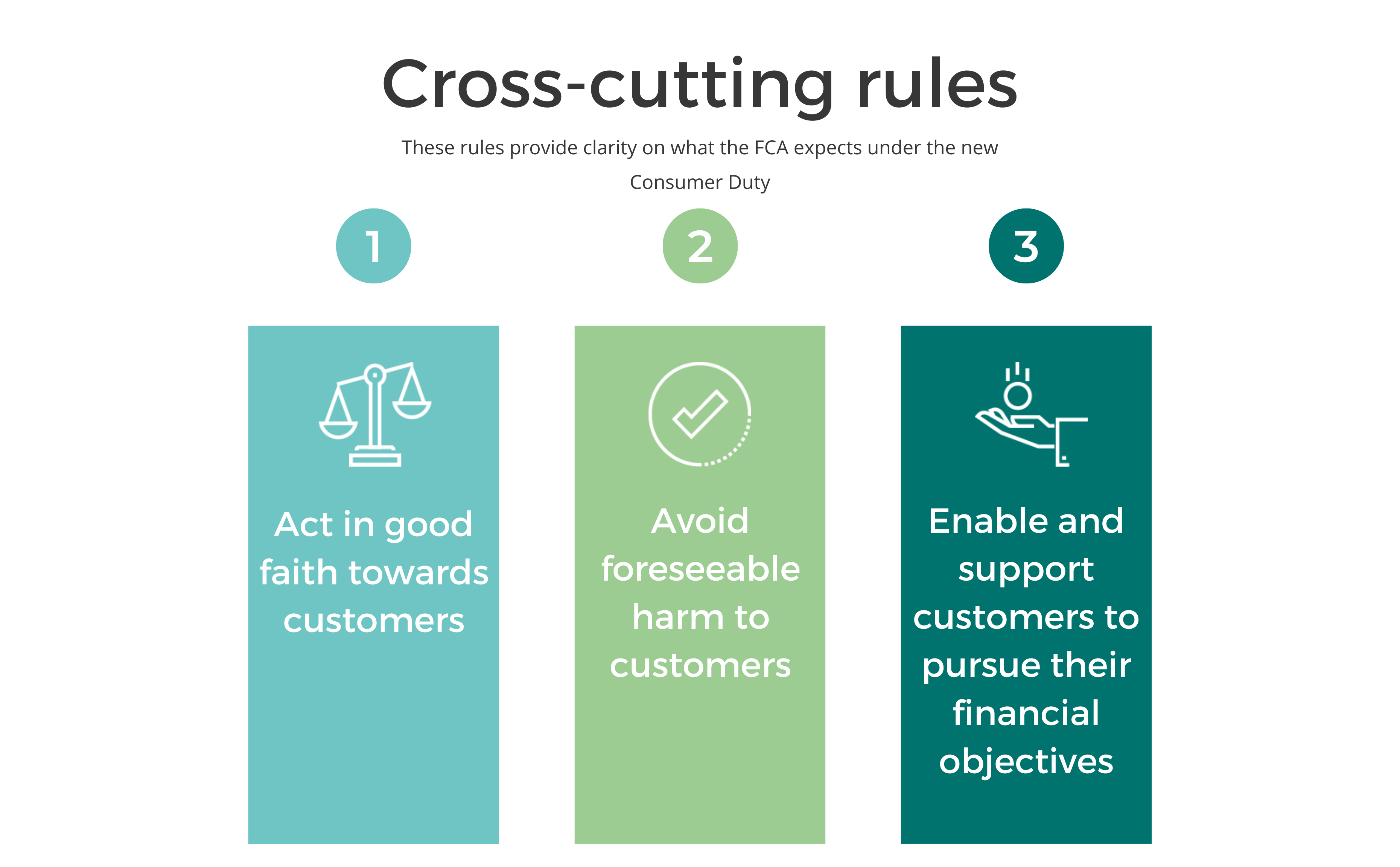

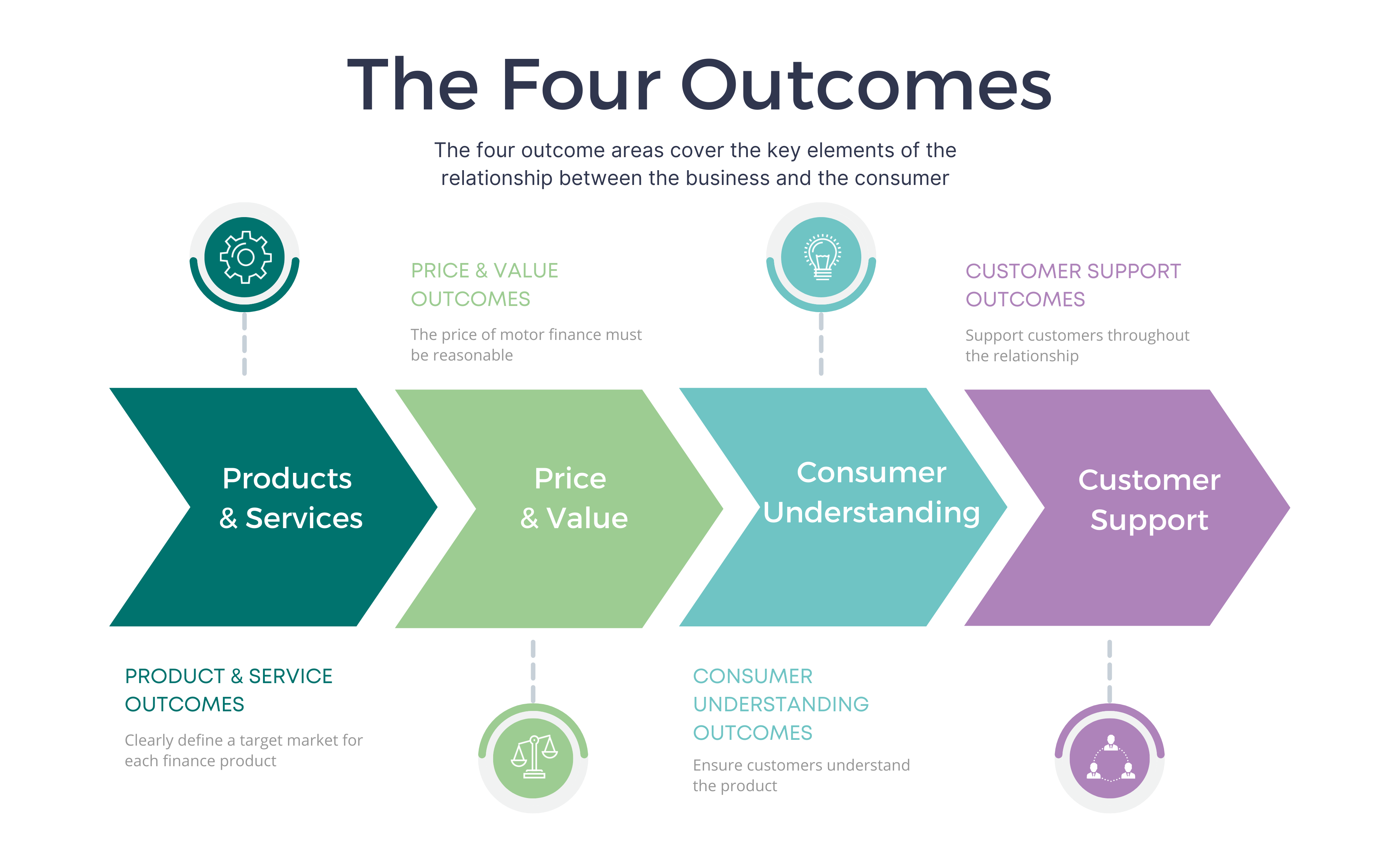

The FCA expects the Duty to be reflected in the strategies, governance, leadership and people policies of all regulated firms. In the motor retail space, this applies to car dealers and finance providers and can be distilled down to three main areas: The Consumer Principle, Cross-Cutting Rules, and Four Outcomes.

Meeting Consumer Duty Requirements

How the right technology can help automotive dealers and lenders deliver good outcomes for customers and meet their regulatory requirements.

The new Consumer Principle sets a higher standard than the previous standard of 'treating customers fairly'. The overarching principle requires firms to take responsibility for serving consumers' interests and delivering good outcomes for customers. Consumers will remain responsible for the decisions they make, but firms must use more judgement when considering the impact of their actions on outcomes for consumers.

The Consumer Principle is designed to lead to a "major shift in financial services", by placing the emphasis on outcomes. Financial services firms will be required to comply with the new rules from 31 July 2023.

The FCA has prepared guidance on how to prepare an implementation plan with advice on what you need to do and when during the implementation period.

Product Enhancements

To to help motor finance providers in fulfilling their responsibilities under the new Consumer Duty, we’ve upgraded our customer journey to include a series of enhancements aimed at helping lenders and dealers meet the new requirements and fulfil the four outcome areas.

Lender Specific Data: The application process now includes a bespoke page listing all the relevant information on the specific finance product chosen by the consumer. Product information is provided by the lender, helping to ensure the product is being introduced in the right way.

Lender Product Videos: This feature allows lenders to supply product information videos explaining the differences and benefits of each finance product, making certain that the product is being introduced properly.

Suitability Assessments: To establish that the customer understands the product, we've included a series of questions, specific to that finance product and provided by the lender, which the customer must answer before proceeding to the application. If the customer does not understand the product, they would be referred to the retailer to offer support in finding a suitable product for their needs.

Support Signposting: We've introduced signposting to government financial advice as well as the lender's own support resources at key points i the journey to assist the consumer, particularly vulnerable customers, in making an informed decision.

Reduce Rejections: Lenders have very specific rules about when, how and to whom they will offer finance. Where we know the specific rules of a lender(for example, lenders who won't lend to taxi drivers), we will intercept this application in the dealer platform before it is sent to the lender, This allows the retailer to support the consumer with finding a lender that better meets their needs and avoids a rejection - a bad outcome for the consumer the retailer and the lender.

Consumer Self-Serve

In recent years, there has been a growing emphasis on consumer protection in the financial services industry. The introduction of new regulations such as Consumer Duty has placed greater responsibilities on firms to act in the best interests of their customers. One area where this is particularly important is in motor finance, where customers may not fully understand the products and services they are offered.

In recent years, there has been a growing emphasis on consumer protection in the financial services industry. The introduction of new regulations such as Consumer Duty has placed greater responsibilities on firms to act in the best interests of their customers. One area where this is particularly important is in motor finance, where customers may not fully understand the products and services they are offered.

The regulations require firms to take a more proactive approach to consumer protection, by putting the customer at the heart of their business and ensuring that products and services throughout the customer journey are designed to meet consumer needs. The goal of these new regulations is to make financing a new car as transparent as possible for consumers.

By allowing customers to self-serve, firms can ensure that they are meeting these requirements, as customers are able to make their own choices about the products and services they want. This can also help build trust between businesses and their customers, as customers are more likely to feel that they have been treated fairly and with respect and helps to reduce the risk of mis-selling.

Mis-selling is a serious issue in the financial services industry and can occur when customers are sold products that are not suitable for their needs. Allowing customers to self-serve, dealers can ensure they are not pressuring customers into buying products that they do not need, and that customers are making choices based on their own needs and circumstances, protecting customers from financial harm.

Customer self-service is becoming increasingly popular in the motor finance industry as it allows customers to have greater control over their accounts and transactions, as well as provides a more convenient and faster service. The consumer self-serve solution provided within iVendi’s Connected Retailing Platform provides customers with a suite of tools delivering choice, visibility and transparency, allowing customers to make informed financial decisions with confidence. The solution offers product suitability assessments, informative product videos, the ability to compare multiple finance products and finance lenders, and an audit trail of transactional activity.

These tools give dealers confidence that consumers are fully informed about the products they are purchasing and can make effective decisions that are in their best interests. By embracing customer self-service, dealers can demonstrate their commitment to increasing consumer and reducing consumer harms protection and ensure that they are meeting their regulatory obligations.

Management Information

Under the new Consumer Duty, financial services firms will need to assess and evidence how they are acting to deliver good outcomes for consumers throughout the lifecycle of the products and services they provide to them. Firms will need to ensure their data strategies will be able to identify, monitor, evidence and stand behind the outcomes their customers experience.

Under the new Consumer Duty, financial services firms will need to assess and evidence how they are acting to deliver good outcomes for consumers throughout the lifecycle of the products and services they provide to them. Firms will need to ensure their data strategies will be able to identify, monitor, evidence and stand behind the outcomes their customers experience.

Rob Severs, Senior VP Product and Insight at iVendi, emphasised the importance of monitoring essential metrics over the longer term to prove that customer needs were being put first.

“As the new Consumer Duty rolls out, much more responsibility is going to be placed on retailers to track consumer activity along every step of the finance journey”, says Severs.

"Management Information (MI) will play a crucial role in helping both lenders and retailers prove compliance and continuous improvement in Consumer Duty. It provides the data and insights necessary for senior managers to understand how good vehicle buyer outcomes are being delivered and where improvements need to be made.”

MI provides businesses with a clear understanding of how their customers interact with their products and services. This data can help senior managers identify areas where they need to improve customer outcomes, identify trends, and ensure that their products and services meet consumer needs.

To meet the Consumer Duty regulation requirements, firms need to have accurate and up-to-date MI that should include data on customers interactions, customer journeys, customer complaints, and customer satisfaction levels. Businesses should also use this data to assess the effectiveness of their processes, procedures and products.

Most retailers who are operating with a multi-lender panel, are very likely to be submitting applications and checks individually to those lenders. Relying on separate processes and systems leaves too much room for error - something the FCA want to avoid when it comes to consumers' private information - and easy to do when running the same information through multiple systems.

Through our Connected Retailing Platform, dealers can compile, track and report on MI. The platform also provides dealers with additional data such as audit trails that capture and demonstrate compliant selling across a panel of lenders, data on market finance rates to ensure dealer offerings remain competitive, and sufficient insight across all their lenders partners to produce accurate representative examples.